In The Prize, Daniel Yergin laid out the argument that volatility (not high prices) of oil in the early 1980s was caused by financial speculation. The primary means of speculation was through derivatives. The NYMEX had then recently introduced future contracts and, according to Yergin, the story goes that guys like T. Boone Pickens made a small fortune off playing the volatility.

T. Boone had dabbled in cattle and cattle feed and so was well versed in futures trading. Flash forward 30-something years and we see a parabolic drop in oil prices. It is a straight line, so to speak, and reads more like a panic riddled sell-off (drop in demand) than a supply driven increase.

Commentary from Charles Hugh Smith's blog:

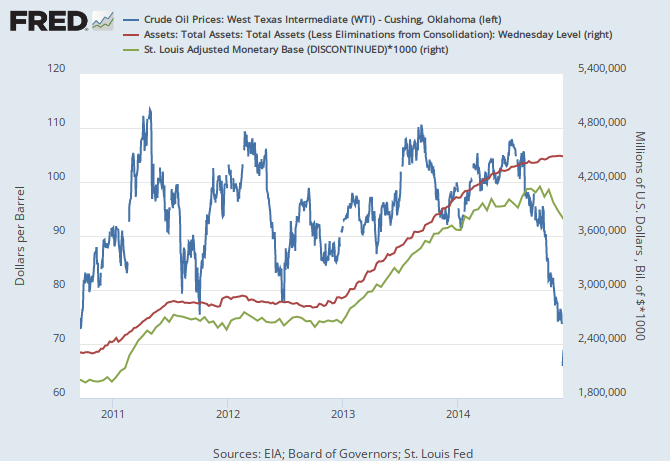

As I said before, the monetary base stops expanding and the Fed ends QE, all as oil prices begin their plunge. Still think the Fed will raise interest rates this coming summer? Does the Fed take the punch bowl away when the party is just getting started?Crowded trades (trades where almost everyone is on one side of the boat) unwind in precisely this sort of freefall. Once the trade has been unwound, however, the selling cascade exhausts itself and insiders who know better start buying. Buying begets buying, shorts start covering, and voila, a retrace that fills open gaps and kisses the 50-day moving average surprises everyone who was confident oil was heading straight down to $40/barrel.